Can a Timeshare Send You to Collections? What Owners Should Know

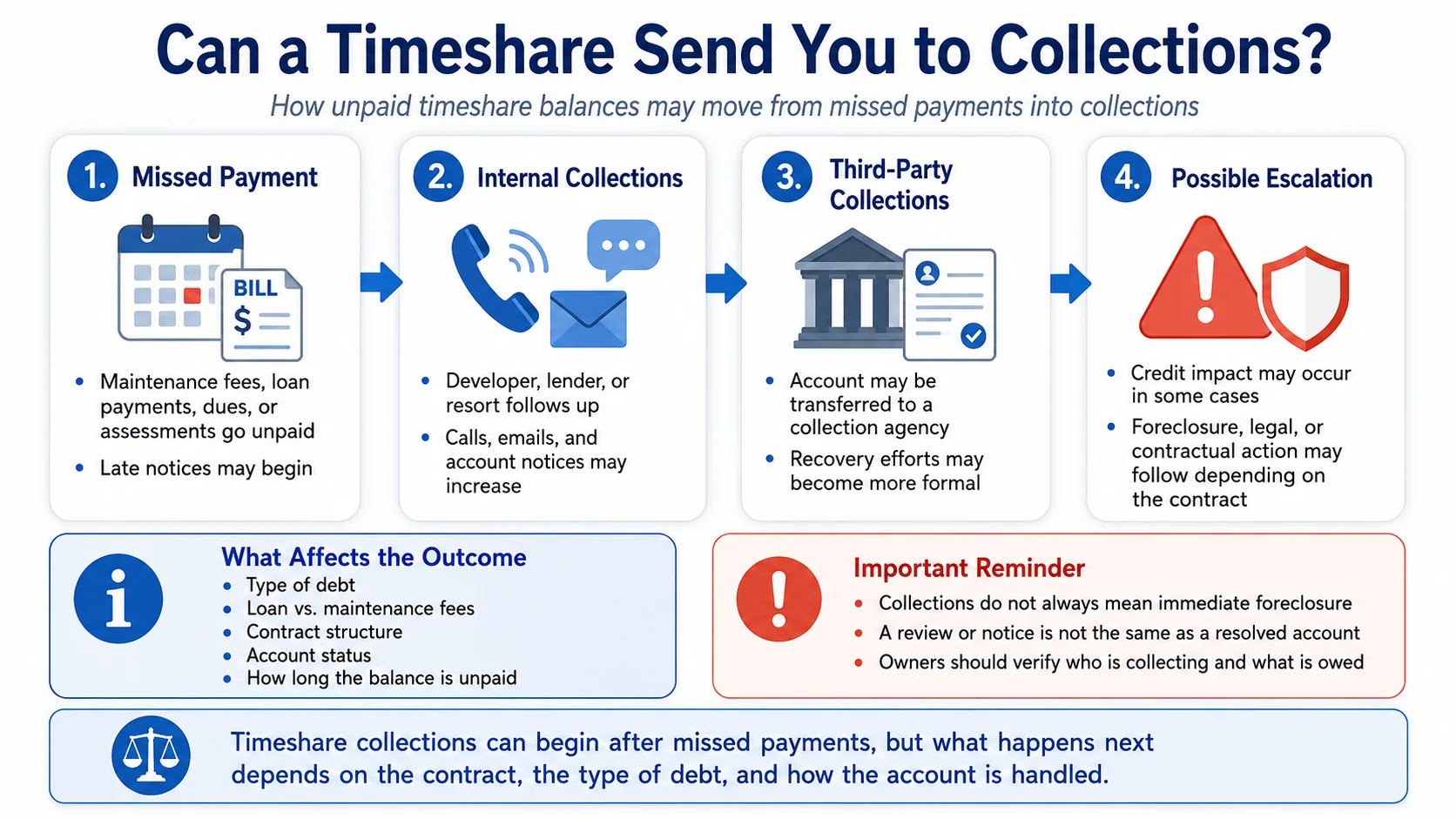

You miss a timeshare payment.

Maybe it is a maintenance fee, loan payment, special assessment, club dues, or another balance tied to the ownership.

At first, it may feel like a late bill.

Then the notices start.

The developer, resort, lender, or management company may contact you about the unpaid balance. If the account remains unresolved, the situation can move from ordinary delinquency into collections.

That is when many owners start asking a more serious question:

“Can a timeshare send me to collections?”

Yes, it can. But what happens next depends on what is unpaid, who is collecting, whether a lender is involved, how the contract is structured, and whether the account stays internal or gets transferred to a third-party collection agency.

The more useful question is not just “Can they send me to collections?”

It is “What type of timeshare debt is being collected, who is handling the account, and what could happen if the balance remains unresolved?”

This guide explains how timeshare collections usually work, why outcomes vary, how credit risk may come into play, and what owners should verify before ignoring notices, making payments, or assuming collections are the final stage.

Quick Answer

Can a Timeshare Send You to Collections?

Yes. If required timeshare payments remain unpaid, the developer, lender, resort, management company, or collection agency may try to collect the balance. This can involve internal collection efforts, third-party agencies, account notices, phone calls, and possible escalation depending on the contract and type of debt.

What happens next depends on whether the missed payment involves a loan, maintenance fees, special assessments, dues, or other charges. Some accounts remain in collections, while others may create credit risk, affect surrender eligibility, or escalate into foreclosure, legal, or contractual action.

Before You Ignore a Collection Notice

Collections Risk Depends on What Is Owed, Who Owns the Debt, and Where the Account Stands.

A timeshare account may be sent to collections for unpaid maintenance fees, loan balances, special assessments, late fees, or other owner obligations. But the real risk depends on the type of debt, account status, notices received, developer or association procedures, credit reporting exposure, and whether foreclosure or legal escalation may also be involved. Before you ignore a letter, stop paying, negotiate blindly, or hire an exit company, the Timeshare Decision Intelligence Report™ helps organize your ownership details, documents, cost exposure, account status, and realistic next-step pathways.

Want a clearer read before responding to collections?

Review the Report Option Or continue reading belowTimeshare Collections Are Not Always the Same Thing

A timeshare account can be “in collections” in more than one way.

Sometimes the developer, resort, lender, management company, or owners’ association is still handling the account internally. Other times, the balance has been transferred to an outside collection agency. In some cases, the unpaid balance is tied to a loan. In others, it may involve maintenance fees, assessments, dues, or other ownership charges.

That distinction matters because the next step may depend on who is collecting, what is owed, and how the debt is structured.

Important Distinction

Collections Can Mean Different Things Depending on What Is Unpaid

A missed loan payment, unpaid maintenance fee, special assessment, or account charge may not be handled the same way. Before deciding what to do next, identify what balance is being collected, who is collecting it, and whether the account is still internal or has been transferred to a third-party agency.

Internal Collections vs. Third-Party Collections

Once a timeshare account becomes delinquent, the first question is usually who is handling the account now?

That matters because internal collections and third-party collections can feel different, move at different speeds, and create different next steps for the owner.

If the account is still internal, the developer, resort, lender, management company, or owners’ association may still be trying to recover the balance directly. If the account has been transferred to a collection agency, the process may become more formal and focused primarily on recovering the balance.

Earlier Stage

Internal Collections

The developer, resort, lender, management company, or owners’ association is still handling the account directly. Communication may include notices, calls, late fees, payment requests, or account-resolution discussions.

Escalated Stage

Third-Party Collections

The balance has been transferred, assigned, or placed with an outside collection agency. Communication may become more formal, and the agency may focus on collecting the balance rather than explaining broader ownership or exit options.

The shift from internal to third-party collections does not automatically mean foreclosure, a lawsuit, or credit reporting has already happened. But it does mean the owner should verify the balance, confirm who is collecting, and understand what type of obligation is involved.

Why Timeshare Collections Outcomes Vary

Timeshare collections do not follow one fixed path.

What happens next depends on the structure of the account, the type of debt involved, and how the developer, lender, resort, or collection agency chooses to handle the balance.

A missed loan payment may be treated differently from unpaid maintenance fees. A special assessment may be handled differently from club dues. An account that is only recently delinquent may create different options than one that has been unpaid for months or already transferred to a third-party agency.

Timing also matters.

Early-stage collections may leave more room to clarify the balance, request documentation, discuss payment options, or understand whether any surrender or exit path remains available. Long-term delinquency can make the situation harder to unwind, especially if late fees, interest, collection costs, credit reporting, foreclosure notices, or legal pressure are added.

The key point is that collections are not just about whether money is owed.

They are about what kind of obligation is unpaid, who is collecting it, how long it has been unresolved, and what the contract allows next.

Owner Risk

Collections Can Affect More Than the Past-Due Balance

Once a timeshare account enters collections, the issue may affect more than the amount currently owed. Collections activity can influence account standing, credit exposure, deed-back or surrender eligibility, transfer options, and whether the matter escalates into foreclosure, legal, or contractual action. Ignoring the notice can make it harder to understand which options are still available.

Free Ownership Review Preview

Not Sure What Matters Most in Your Timeshare Situation?

Timeshare decisions can depend on several factors at once, including ownership type, loan status, annual fees, usage fit, transfer rules, surrender options, resale difficulty, and account standing. The free Ownership Risk Profile™ Preview can help you identify which issues may deserve closer attention before you choose a next step.

Want a quick read on your ownership factors?

Try the Free Preview Free preview • Educational decision support • No exit-company sales pitchWhat to Confirm Before You Respond

A collection notice should not be ignored, but it also should not be answered blindly.

Before making a payment, disputing a balance, calling the agency, or assuming the account cannot be resolved, slow down and confirm the basics. You need to know who is collecting, what type of balance is involved, whether the amount is accurate, and what the account status means for future fees, surrender options, credit exposure, or possible escalation.

Action Step

Verify the Collection Details Before Taking Action

Before responding to a timeshare collection notice, gather the basic facts. The right next step depends on whether the balance involves a loan, maintenance fees, assessments, dues, or another contractual obligation.

Confirm whether the account is still internal or with a third-party collection agency.

Identify what type of balance is being collected: loan, maintenance fees, dues, assessments, or other charges.

Request or review an itemized balance showing fees, interest, late charges, collection costs, or other additions.

Check whether the account has been reported to credit bureaus, may be reported later, or is still being handled internally.

Ask whether the delinquency affects deed-back, surrender, resale, transfer, or other exit options.

Keep copies of notices, emails, payment records, account statements, and written responses.

Quick win: Before paying or disputing anything, identify who is collecting, what balance is being collected, and whether the account status affects future exit or surrender options.

How Timeshare Collections May Affect Your Credit

One of the biggest concerns is whether timeshare collections can damage your credit.

The answer is: it depends.

Credit impact may depend on what type of balance is unpaid, whether a lender is involved, whether the developer reports delinquency, and whether a third-party collection agency reports the account. A financed timeshare loan may be handled differently from unpaid maintenance fees or assessments.

Some collection activity may appear on credit reports. Some may not. Some accounts may remain internal for a period of time before anything is reported. Others may move to a third-party agency with different reporting practices.

That uncertainty is why owners should not assume collections are harmless simply because nothing has appeared on a credit report yet.

Even when credit reporting is limited, unresolved collections can still create problems. The account may remain out of good standing, additional fees may continue, surrender or deed-back eligibility may be affected, and the issue may escalate if the balance remains unpaid.

The practical takeaway is simple: credit impact is only one part of the risk. Account status, contract obligations, collection activity, and future exit options may matter just as much.

What Are Timeshare Collections?

Timeshare collections refer to the process used by developers or lenders to recover unpaid balances after required payments are missed. This typically includes ongoing efforts to contact the owner, notify them of the delinquency, and request payment.

The process may be handled internally at first, with the developer managing outreach and account follow-up. If the balance remains unresolved, the account may be transferred to a third-party collection agency that specializes in recovering debt.

Not all collections situations are the same. Some involve unpaid loan balances tied to financing, while others relate only to maintenance fees or contractual charges. These differences can affect how the account is handled and what actions may follow.

Because of this variability, collections can range from relatively limited contact attempts to more persistent recovery efforts, depending on the contract and how long the account remains delinquent.

Owner takeaway: A collections notice does not always mean foreclosure, a lawsuit, or credit damage is immediate. But it does mean the account has moved into a more formal recovery stage. The next step depends on what is owed, who is collecting, and whether the account is still internal or with a third party.

❓Frequently Asked Questions

These questions come up often when owners are trying to understand what collections may mean, how serious the situation is, and what to verify before responding.

Bottom Line

A timeshare can be sent to collections when required payments remain unpaid.

What happens next depends on what is owed, who is collecting, whether a loan is involved, how the contract is structured, and how long the account remains unresolved.

Collections do not always mean immediate foreclosure, legal action, or credit damage. But they do mean the account has moved into a more formal recovery stage. Before ignoring notices, making payments, disputing the balance, or assuming an exit option is still available, confirm what is being collected and how the account status affects your next step.

The Wrong Timeshare Exit Move Can Cost More Than the Problem You’re Trying to Solve.

Stopping payments, hiring an exit company, chasing resale promises, requesting a surrender, or transferring ownership can all lead to very different outcomes depending on your contract, loan status, fees, account standing, documents, and developer rules. The Timeshare Decision Intelligence Report™ helps organize those details so you can see which paths appear realistic before you commit to the wrong move.

Get the Timeshare Decision Intelligence Report™ Customized ownership review • Decision-support report • No exit-company sales pitchIndependent decision support. This is not legal advice, contract cancellation, an exit service, a resale service, lender negotiation, or a promise that your timeshare can be exited.

Related Guides

If your timeshare account is in collections, these guides can help you understand what may happen next and how missed payments can affect surrender, foreclosure, credit, or exit options.

Timeshare Debt Collection: What Owners Should Know Before Paying

If your account is already with a collector, understand what the collection balance covers, whether paying it resolves only the debt, and whether the timeshare ownership may still remain active.

What Happens If You Stop Paying Timeshare Maintenance Fees?

Review what can happen when maintenance fees go unpaid and why stopping payments is different from a confirmed release.

What Is a Timeshare Deed-Back Program?

Understand why deed-back and surrender programs often require the account to be current and in good standing before the developer will review a return request.

Can You Sell a Timeshare Back to the Developer?

Learn why developer buybacks are usually unrealistic and how collections can complicate resale, surrender, or transfer options.

Can a Timeshare Put a Lien on Your House?

Understand why lien risk usually starts with the timeshare interest itself, but unpaid balances and judgments can create broader financial concerns.