Timeshare Debt Collection: What Owners Should Know Before Paying

You receive a timeshare collection notice.

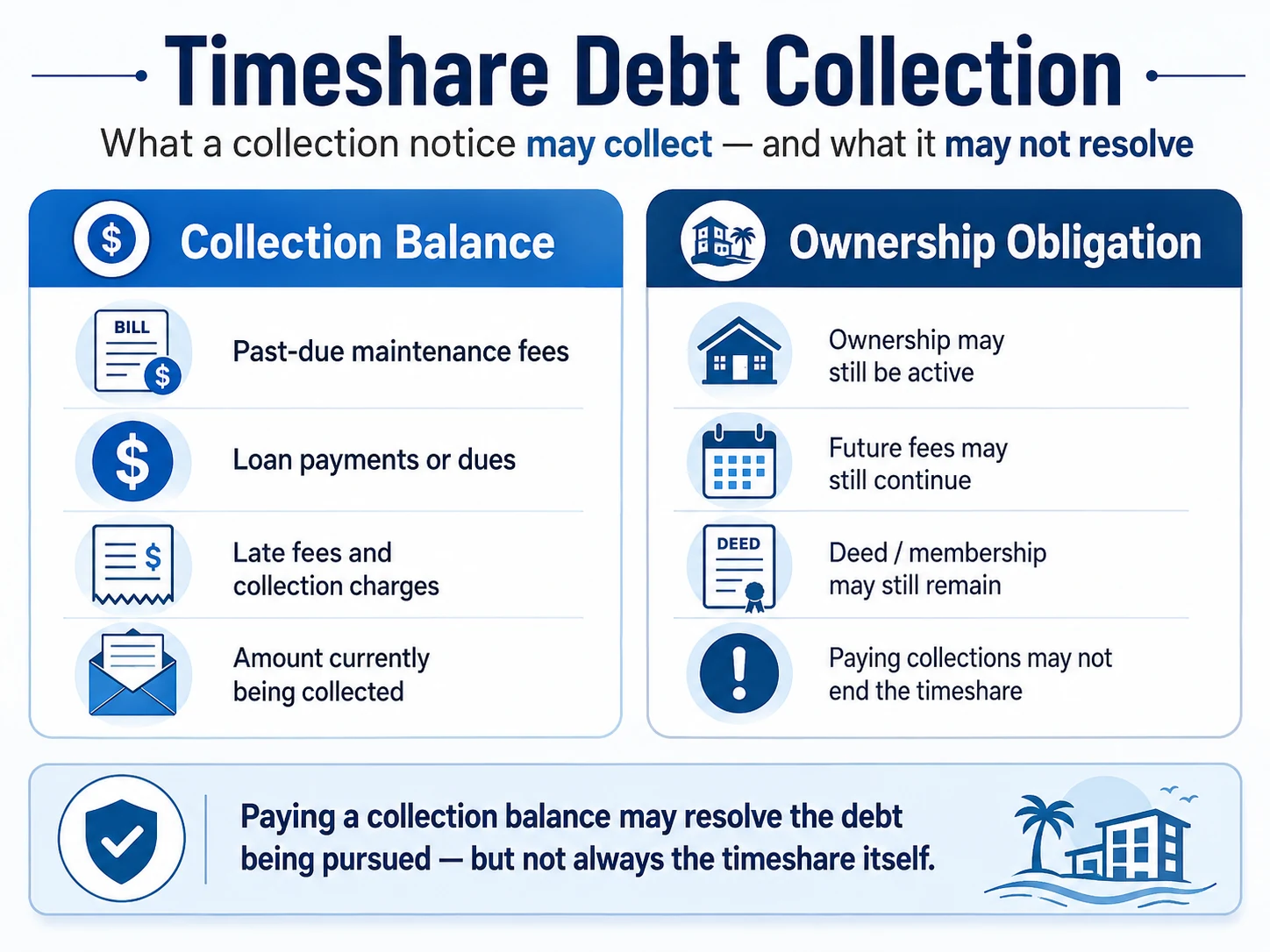

The balance may involve unpaid maintenance fees, loan payments, special assessments, late charges, collection costs, or another amount connected to the ownership.

At first, the question may seem simple:

“How do I deal with this collection balance?”

But with timeshares, there is often a second question that matters just as much:

“Does paying or settling this debt actually resolve the timeshare?”

That distinction is important.

A collection notice usually focuses on money that is already past due. It may not explain whether the ownership, contract, deed, membership, or future fee obligation is still active. In some cases, paying the collection balance may resolve the amount being pursued but leave future maintenance fees, assessments, or ownership responsibilities in place.

The more useful question is not just “What do I owe?”

It is “What is being collected, who is collecting it, and whether the timeshare obligation continues after this balance is paid, settled, disputed, or ignored?”

This guide explains how timeshare debt collection works, what owners should verify before paying, and why resolving a collection balance is not always the same as resolving the timeshare itself.

Quick Answer

What Happens in Timeshare Debt Collection?

Timeshare debt collection means a developer, resort, lender, homeowners association, servicing company, law office, or collection agency is trying to recover an unpaid balance tied to the ownership. That balance may involve loan payments, maintenance fees, assessments, late fees, interest, or collection charges.

Paying or settling a collection balance may resolve the amount being collected, but it does not always end the timeshare ownership or stop future obligations. Before paying, owners should confirm what debt is being collected, who is collecting it, what period it covers, and whether the ownership remains active after the balance is resolved.

Before You Pay a Collection Demand

Timeshare Collection Debt Should Be Reviewed Before You React.

A timeshare collection demand may involve unpaid maintenance fees, loan balances, special assessments, late charges, legal fees, foreclosure costs, or amounts transferred to a third-party collector. Before you pay, ignore the notice, dispute blindly, accept a settlement, or hire an exit company, the Timeshare Decision Intelligence Report™ helps organize your ownership details, account status, documents, cost exposure, collection risk, and realistic next-step pathways.

Want a clearer read before responding to a collection demand?

Review the Report Option Or continue reading belowA Collection Balance Is Not Always the Same as the Ownership

A timeshare collection notice usually focuses on money that is already past due.

But it may not answer the bigger question:

Does the ownership itself still continue?

That distinction matters because paying, settling, or disputing a collection balance may resolve one debt while future fees, assessments, dues, or ownership responsibilities continue under the contract.

Important Distinction

Paying the Debt May Not End the Timeshare

A collection agency may be trying to recover a specific balance, such as unpaid fees, loan payments, assessments, late charges, or collection costs. But unless the ownership is formally transferred, surrendered, foreclosed, canceled, or otherwise released, the timeshare obligation may still remain active.

What Timeshare Debt Collection Means

Timeshare debt collection means an unpaid balance tied to the ownership is being pursued more formally.

That balance may be handled by the developer, resort, homeowners association, lender, servicing company, law office, or a third-party collection agency. The collector may be trying to recover a specific past-due amount, but that does not always explain the full status of the timeshare.

This is where owners need to be careful.

A collection notice may show the amount being pursued now. It may not explain whether the ownership is still active, whether future fees can continue, or whether the account requires a separate surrender, transfer, foreclosure, cancellation, or release process.

Before deciding what to do next, identify two things clearly:

What debt is being collected?

Does the timeshare obligation continue after that debt is resolved?

What Types of Timeshare Debt May Be Sent to Collections?

Not all timeshare debt collection comes from the same kind of balance.

Some notices involve missed loan payments. Others involve unpaid maintenance fees, special assessments, dues, late fees, interest, collection costs, or administrative charges. The source of the debt matters because each type of balance can lead to different consequences.

A loan balance may involve a lender or servicer. Maintenance fees may involve the resort, association, or management company. Special assessments may be tied to a specific property cost or ownership obligation. Collection charges may be added after the account has already become delinquent.

The notice should show what balance is being pursued, but it may not fully explain whether the timeshare itself remains active.

That is the practical issue: paying one collection balance may not resolve every obligation connected to the ownership.

Owner Risk

Paying Collections May Not Resolve the Timeshare Itself

The biggest risk is assuming that paying or settling a collection balance ends the entire timeshare obligation. If the ownership remains active, future maintenance fees, assessments, dues, late charges, or collection activity may continue. Before paying, owners should confirm whether the payment resolves only the debt being collected — or whether it is connected to a written release, transfer, surrender, foreclosure, cancellation, or other formal resolution of the ownership.

Free Ownership Review Preview

Not Sure What Matters Most in Your Timeshare Situation?

Timeshare decisions can depend on several factors at once, including ownership type, loan status, annual fees, usage fit, transfer rules, surrender options, resale difficulty, and account standing. The free Ownership Risk Profile™ Preview can help you identify which issues may deserve closer attention before you choose a next step.

Want a quick read on your ownership factors?

Try the Free Preview Free preview • Educational decision support • No exit-company sales pitchWhat to Confirm Before You Pay or Respond

Before paying, settling, disputing, or ignoring a timeshare collection notice, slow down and separate the debt from the ownership.

A collection agency may be focused on a specific balance. The developer, resort, lender, HOA, or management company may still control other parts of the account. That means the collection notice may not tell you whether future fees can continue, whether the timeshare is still active, or whether a separate release, surrender, transfer, foreclosure, or cancellation process is required.

The goal is to understand what the payment would resolve — and what may still remain afterward.

Action Step

Verify the Debt and the Ownership Status Before Paying

Before responding to a timeshare debt collection notice, confirm what the notice covers and what it does not cover. The most important issue is whether payment resolves only the collection balance or also affects the underlying timeshare obligation.

Confirm who is collecting: developer, resort, HOA, lender, servicer, law office, or collection agency.

Ask for an itemized breakdown of the debt, including fees, interest, late charges, or collection costs.

Identify whether the balance involves a loan, maintenance fees, assessments, dues, or added charges.

Ask what billing period or account period the collection balance covers.

Confirm whether the ownership, deed, points contract, or membership remains active after payment.

Get all payment, settlement, release, transfer, surrender, or account-closure terms in writing before sending money.

Quick win: Before paying a collection balance, ask one direct question in writing: “Does this payment resolve only the debt being collected, or does it also end my future timeshare obligations?”

Does Paying Timeshare Collections End the Ownership?

Paying or settling a timeshare collection balance may resolve the amount being collected, but it does not automatically end the timeshare ownership.

That is the issue many owners miss.

A collection balance may be tied to one specific debt, such as missed loan payments, unpaid maintenance fees, a special assessment, late fees, interest, or collection costs.If the underlying ownership remains active, future charges may still continue even after the current balance is paid.

Before paying, ask what the payment actually resolves.

Does it only satisfy the past-due balance? Does it bring the account current? Does it settle a specific collection claim? Or does it include a written release, surrender, transfer, foreclosure, cancellation, or other formal resolution of the ownership?

Those are very different outcomes.

The safest position is simple: do not assume payment ends the timeshare unless the written terms clearly say that future ownership obligations are resolved.

Can Timeshare Debt Collection Affect Your Credit?

Timeshare debt collection may affect your credit, but the outcome depends on how the debt is structured and reported.

A financed timeshare loan may be more likely to create credit exposure because missed loan payments can be treated differently from unpaid fees. A third-party collection agency may also report the account depending on its practices and the nature of the debt.

Maintenance fees, assessments, dues, and other ownership-related charges can be less predictable. Some accounts may be reported. Others may remain internal for a period of time. Some may create credit issues only after the account is transferred, escalated, or handled by a collector that reports to credit bureaus.

The key point is that credit reporting is not the only risk.

Even if the collection account does not appear on a credit report right away, the ownership may still be active, the balance may grow, and unresolved account status may affect surrender, deed-back, resale, transfer, or future exit options.

Owner takeaway: A timeshare collection payment may resolve one balance, but it does not automatically resolve the ownership. Before paying or settling, confirm whether future fees, dues, assessments, or contract obligations can continue after the collection account is addressed.

❓Frequently Asked Questions

These questions come up often when owners receive a timeshare collection notice and are trying to understand what the debt means, what payment resolves, and whether the ownership is still active.

Bottom Line

Timeshare debt collection usually means an unpaid balance is being pursued.

But the collection balance is not always the full issue.

A notice may involve loan payments, maintenance fees, assessments, late fees, interest, or collection costs. Paying or settling that balance may resolve the debt being collected, but it does not automatically end the timeshare ownership or stop future obligations.

Before paying, settling, disputing, ignoring the notice, or hiring outside help, confirm what is being collected, who is collecting it, and whether the ownership remains active after the current balance is resolved.

The Wrong Timeshare Exit Move Can Cost More Than the Problem You’re Trying to Solve.

Stopping payments, hiring an exit company, chasing resale promises, requesting a surrender, or transferring ownership can all lead to very different outcomes depending on your contract, loan status, fees, account standing, documents, and developer rules. The Timeshare Decision Intelligence Report™ helps organize those details so you can see which paths appear realistic before you commit to the wrong move.

Get the Timeshare Decision Intelligence Report™ Customized ownership review • Decision-support report • No exit-company sales pitchIndependent decision support. This is not legal advice, contract cancellation, an exit service, a resale service, lender negotiation, or a promise that your timeshare can be exited.

Related Guides

If your timeshare account is already in debt collection, these guides can help you understand what may happen next, what payment may or may not resolve, and how your ownership structure affects your options.

Can a Timeshare Send You to Collections?

Understand how missed timeshare payments may move from internal notices to third-party collections and possible escalation.

What Happens When Timeshare Maintenance Fees Go to Collections?

Review how unpaid maintenance fees may be handled differently from loans, assessments, or other timeshare-related debts.

Can You Exit a Timeshare Without Ruining Your Credit?

Learn why credit impact depends on the type of debt, reporting practices, account status, and how the ownership is resolved.

How to Get Out of a Timeshare: Legal and Practical Options

Step back and compare the broader exit paths that may apply, including resale, transfer, developer programs, negotiated resolution, and structured review.

Timeshare Foreclosure: What Owners Should Know

See how unresolved balances may escalate beyond collections in some cases and why foreclosure risk depends on the contract, ownership type, and enforcement process.