Can You Exit a Timeshare Without Ruining Your Credit?

You want out of the timeshare.

But you do not want the exit process to damage your credit.

That concern is valid.

Some owners can leave a timeshare without credit damage when payments stay current and the exit follows an approved path. Others run into problems when payments stop, a loan goes into default, maintenance fees are sent to collections, or the account moves toward foreclosure or legal enforcement.

The key issue is not simply “Can I exit?”

It is “Which exit path creates the least credit risk for my situation?”

That depends on your ownership structure, whether there is an active loan, whether fees are current, whether the developer offers a surrender or deed-back option, and whether the account has already moved into collections.

This guide explains how different exit paths can affect credit risk, which options are generally lower risk, and what owners should verify before stopping payments, relying on an exit company, or assuming a timeshare exit will be credit-safe.

Quick Answer

Can You Exit a Timeshare Without Ruining Your Credit?

Yes, it may be possible to exit a timeshare without damaging your credit, but it depends on how the exit is handled. Credit risk is usually lower when payments stay current, any loan is addressed, and the ownership is transferred, surrendered, rescinded, or resolved through an approved written path.

Credit risk usually increases when payments stop without a plan, a financed loan goes into default, unpaid maintenance fees move to collections, or the account escalates into foreclosure, legal action, or reported delinquency. The safest starting point is to understand your loan status, fee status, account standing, and available exit options before choosing a path.

Before You Choose an Exit Path

Getting Out Without Credit Damage Depends on the Details of the Account.

Credit risk can depend on whether you have a timeshare loan, unpaid maintenance fees, collection activity, foreclosure exposure, late notices, or developer repayment procedures. Before you stop paying, assume your credit is safe, hire an exit company, or accept a transfer promise, the Timeshare Decision Intelligence Report™ helps organize your ownership details, account status, documents, cost exposure, and realistic next-step pathways.

Want a clearer read before making a credit-sensitive exit decision?

Review the Report Option Or continue reading belowCredit Risk Comes From the Exit Path, Not the Desire to Exit

Wanting out of a timeshare does not automatically damage your credit.

The credit risk usually appears when the exit path creates a payment problem, default, collection account, foreclosure event, or reported delinquency. That is why two owners can both be trying to exit, but face very different credit outcomes.

One owner may stay current while completing a developer-approved surrender, resale, transfer, or rescission. Another may stop paying before a plan is in place and end up with collections or default activity.

That difference matters more than the word “exit.”

Important Distinction

Exiting Does Not Usually Hurt Credit — Default Can

A timeshare exit is not automatically a credit event. Credit risk usually comes from missed payments, loan default, collections, foreclosure, legal judgments, or other reported account activity. The safer path is usually the one that resolves the ownership while keeping payment obligations current or clearly addressed in writing.

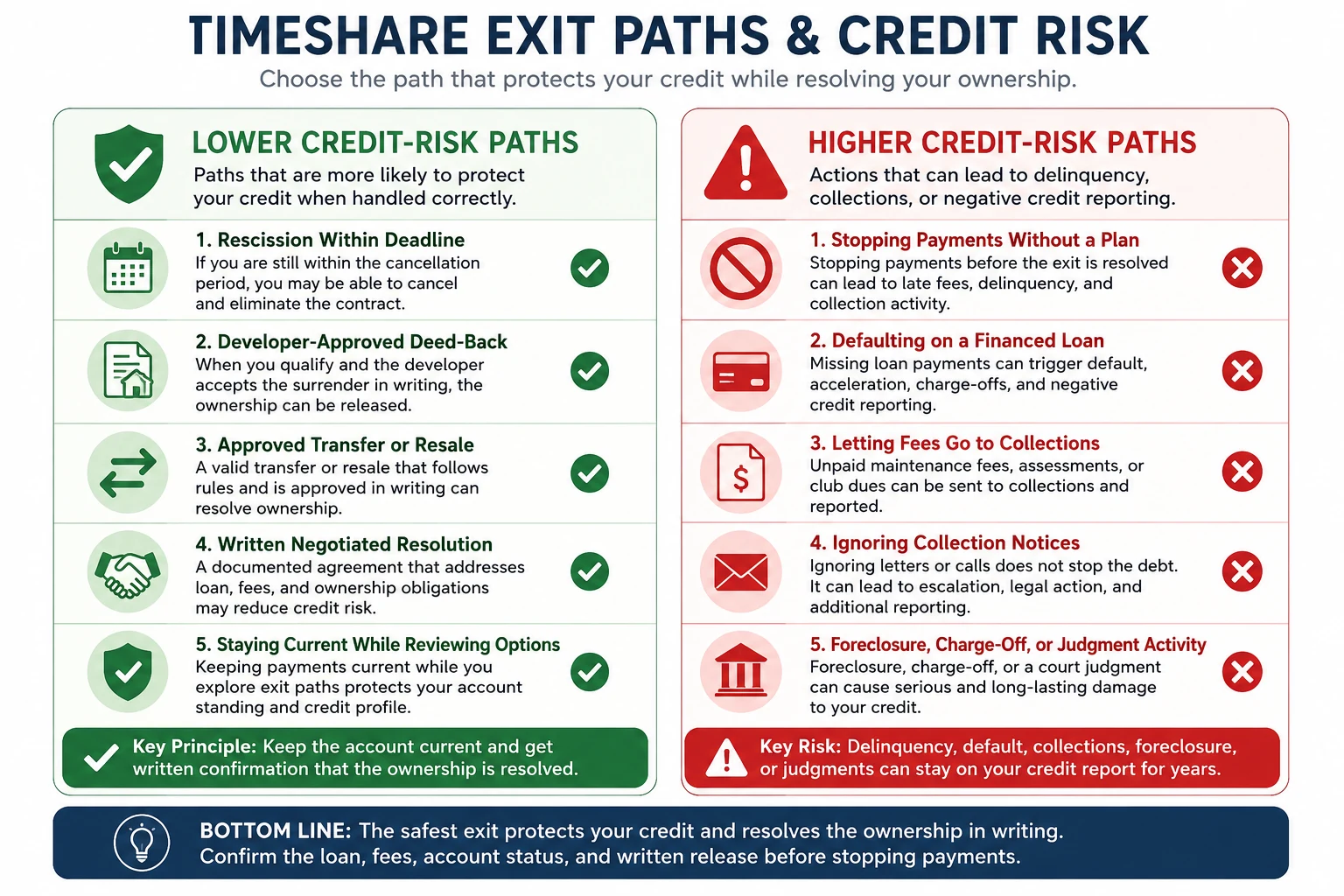

Lower-Risk vs. Higher-Risk Exit Paths

Not every exit path creates the same credit exposure.

The lower-risk paths usually have one thing in common: the account stays current, the developer or lender recognizes the resolution, and the owner gets written confirmation of what has been transferred, surrendered, canceled, or released.

The higher-risk paths usually begin when payments stop before the ownership is resolved.

That does not mean every missed payment leads to credit damage. But once default, collections, foreclosure, or reported delinquency enters the picture, the exit path can become harder to control.

Lower Credit-Risk Paths

Structured or Approved Exits

These paths are generally less likely to create credit damage when payments remain current and the exit is completed through a recognized process.

- Rescission within the legal cancellation window

- Developer-approved deed-back or surrender

- Approved resale or transfer

- Negotiated written resolution

- Staying current while reviewing options

Higher Credit-Risk Paths

Default or Unresolved Payment Problems

These paths may create more credit exposure because the account can become delinquent, reported, transferred to collections, or escalated.

- Stopping payments before a plan is in place

- Defaulting on a financed timeshare loan

- Letting maintenance fees move to collections

- Ignoring collection notices

- Foreclosure, charge-off, or judgment activity

The safest path is usually not the one that promises the fastest exit. It is the one that clearly addresses the loan, fees, account standing, and written release before credit-damaging activity begins.

Why Financing Status Matters

The biggest credit distinction is whether the timeshare is financed.

If there is an active loan, missed payments may create credit risk more quickly because the account may be reported like other consumer debt. Late payments, default, charge-off, acceleration, or foreclosure-related activity may affect credit depending on how the lender or developer reports the account.

If the timeshare is paid off, the credit risk may be less direct — but it is not always gone.

Unpaid maintenance fees, special assessments, club dues, or other charges may still create problems if they move into collections, foreclosure, legal enforcement, or reported account activity. A paid-off timeshare can still create credit risk if the owner stops paying required fees and the account escalates.

That is why “paid off” does not automatically mean “credit-safe.”

The safer question is:

Is there any unpaid or reportable obligation tied to the timeshare, and what happens if it is not resolved?

Owner Risk

Stopping Payments Before the Exit Is Resolved Can Create Credit Risk

The biggest credit risk usually starts when an owner stops paying before the ownership, loan, fees, or account status has been formally resolved. If payments stop too early, the account may become delinquent, move to collections, trigger default activity, or create reporting that is harder to undo later. A promised exit is not the same as a completed release, transfer, surrender, rescission, or written resolution.

Free Ownership Review Preview

Not Sure What Matters Most in Your Timeshare Situation?

Timeshare decisions can depend on several factors at once, including ownership type, loan status, annual fees, usage fit, transfer rules, surrender options, resale difficulty, and account standing. The free Ownership Risk Profile™ Preview can help you identify which issues may deserve closer attention before you choose a next step.

Want a quick read on your ownership factors?

Try the Free Preview Free preview • Educational decision support • No exit-company sales pitchWhat to Confirm Before Choosing an Exit Path

Before you choose an exit strategy, separate the credit question from the ownership question.

A path may sound safe because someone says they can “get you out,” but the real issue is whether the loan, fees, account standing, and future obligations are being handled in a way that avoids default, collections, foreclosure, or reported delinquency.

The goal is not just to exit. The goal is to exit with a clear written path that explains what happens to the ownership, what happens to any unpaid balance, and what activity could be reported.

Action Step

Check the Credit Risk Before You Commit to an Exit Path

Before choosing an exit strategy, confirm how the path affects your payment status, loan balance, maintenance fees, account standing, and future reporting risk. The safest option is usually the one that resolves the ownership without triggering avoidable delinquency.

Confirm whether your timeshare has an active loan or financing agreement.

Check whether maintenance fees, dues, assessments, or other balances are current.

Ask whether the account is current, delinquent, in collections, with a third-party collector, or already reported.

Confirm whether the developer, lender, collector, or servicer reports account activity.

Get written terms for any surrender, deed-back, transfer, resale, settlement, or release.

Avoid stopping payments until you understand what could be reported or escalated.

Quick win: Before choosing an exit path, ask: “What has to stay current, what could be reported, and what written proof shows the ownership is resolved?”

When a Timeshare Exit Is More Likely to Be Credit-Safe

A timeshare exit is more likely to avoid credit damage when the account stays current and the resolution is documented.

That usually means the owner is not relying on silence, delay, or stopped payments as the strategy. Instead, the exit path is tied to something the developer, lender, buyer, transferee, or other authorized party recognizes.

Lower-risk situations may include rescission within the cancellation period, a developer-approved deed-back, an approved transfer or resale, or a written resolution that clearly addresses any loan, fees, and future obligations.

The most important part is written confirmation.

A phone conversation, sales promise, or third-party assurance is not enough if the account later becomes delinquent or reported. The owner needs to know what is being resolved, when responsibility ends, and whether any remaining balance could still be collected or reported.

Owner takeaway: The lowest credit-risk exit is usually the one that keeps payments current or clearly resolves them in writing. Before relying on any exit path, confirm what happens to the loan, fees, account standing, and future ownership obligations.

Why Timing Matters

Timing can make a major difference when credit protection is the goal.

The earlier an owner evaluates their options, the more likely they are to have choices that do not involve delinquency. If payments are still current, the owner may have more room to explore developer programs, approved transfers, resale options, or written resolutions before the account escalates.

Once payments are missed, the situation can become harder to manage.

A late payment may lead to fees. Continued nonpayment may lead to collections. A financed loan may create default or reporting risk. Unpaid maintenance fees may affect account standing, surrender eligibility, or future transfer options.

That is why waiting for the account to become urgent can reduce flexibility.

If credit protection is one of the main goals, the safer approach is to understand the ownership structure before stopping payments, signing with an exit company, or assuming the developer will accept the timeshare back.

❓Frequently Asked Questions

These questions come up often when owners want to exit a timeshare but are worried about credit damage, collections, loan default, or future reporting.

Bottom Line

You may be able to exit a timeshare without ruining your credit, but the path matters.

Credit risk usually comes from missed payments, loan default, collections, foreclosure, legal judgments, or reported delinquency — not from the desire to exit by itself.

The lower-risk approach is usually to stay current while you confirm what exit options are available, whether the loan and fees are addressed, and what written proof shows the ownership has been resolved.

Before stopping payments, paying an outside company, relying on surrender, or assuming your credit is safe, verify the structure of your account and the consequences of the path you are considering.

The Wrong Timeshare Exit Move Can Cost More Than the Problem You’re Trying to Solve.

Stopping payments, hiring an exit company, chasing resale promises, requesting a surrender, or transferring ownership can all lead to very different outcomes depending on your contract, loan status, fees, account standing, documents, and developer rules. The Timeshare Decision Intelligence Report™ helps organize those details so you can see which paths appear realistic before you commit to the wrong move.

Get the Timeshare Decision Intelligence Report™ Customized ownership review • Decision-support report • No exit-company sales pitchIndependent decision support. This is not legal advice, contract cancellation, an exit service, a resale service, lender negotiation, or a promise that your timeshare can be exited.

Related Guides

If you are trying to exit a timeshare without damaging your credit, these guides can help you understand the nearby risks, payment issues, and broader exit paths.

Can a Timeshare Affect Your Credit Score?

Understand when a timeshare can affect credit, including loans, missed payments, collections, foreclosure reporting, and legal judgments.

How to Get Out of a Timeshare: Legal and Practical Options

Compare broader exit paths, including rescission, resale, transfer, deed-back, surrender, negotiated resolution, and structured review.

How to Cancel a Timeshare Contract

Understand when true cancellation may still be available, why rescission deadlines matter, and how post-rescission options usually shift from cancellation to broader exit planning.

What Is a Timeshare Deed-Back Program?

Learn why developer surrender and deed-back programs may be lower-risk when the account qualifies and the release is confirmed in writing.

Timeshare Special Assessments: What They Are and When They Happen

Understand how unexpected assessment charges can increase financial pressure and why unpaid assessments may affect credit risk, collections, or the exit path you choose.

Can a Timeshare Send You to Collections?

Review how missed payments can move into collections and why account status can affect credit risk and future exit options.

Timeshare Debt Collection: What Owners Should Know Before Paying

Understand why paying a collection balance may not always resolve the ownership or stop future fees.