Can’t Afford Your Timeshare Anymore? What to Do Before You Stop Paying

A timeshare can become unaffordable even when the owner is still current on every payment.

The pressure may come from a monthly purchase loan, rising maintenance fees, club dues, special assessments, or an unexpected change in household income. But affordability can also break down when the owner can no longer afford to take the vacations the ownership was meant to provide.

Airfare, driving costs, rental cars, exchange fees, resort charges, all-inclusive fees, meals, parking, taxes, and other trip expenses can make using the timeshare considerably more expensive than the ownership bills alone suggest.

An owner may therefore be able to keep paying for the timeshare while no longer being able to use it in a practical or worthwhile way.

The situation becomes more urgent once payments are missed. Past-due balances may lead to late fees, collections, credit reporting, liens, foreclosure, or other enforcement activity depending on the ownership and obligation involved. Those later stages are addressed in separate guides throughout this site.

The more useful question is not simply:

“Can I still afford the timeshare payment?”

It is:

“Can I afford both to keep this ownership and to use it in a way that provides enough value?”

This guide explains how to identify the source of the financial pressure, review the full ownership and travel costs, evaluate options while they may still be available, and avoid turning an affordability problem into a default or collection problem.

Quick Answer

What Should You Do If You Can’t Afford Your Timeshare?

Start by identifying what is making the ownership unaffordable. The pressure may come from a purchase loan, maintenance fees, club dues, special assessments, travel costs, reduced usage, or an account that is already falling behind.

Then confirm the loan balance, account status, annual obligations, cost of using the ownership, and whether written hardship, surrender, resale, transfer, or payment options remain available. Stopping payments may narrow those options and create separate collection, credit, lien, or foreclosure consequences.

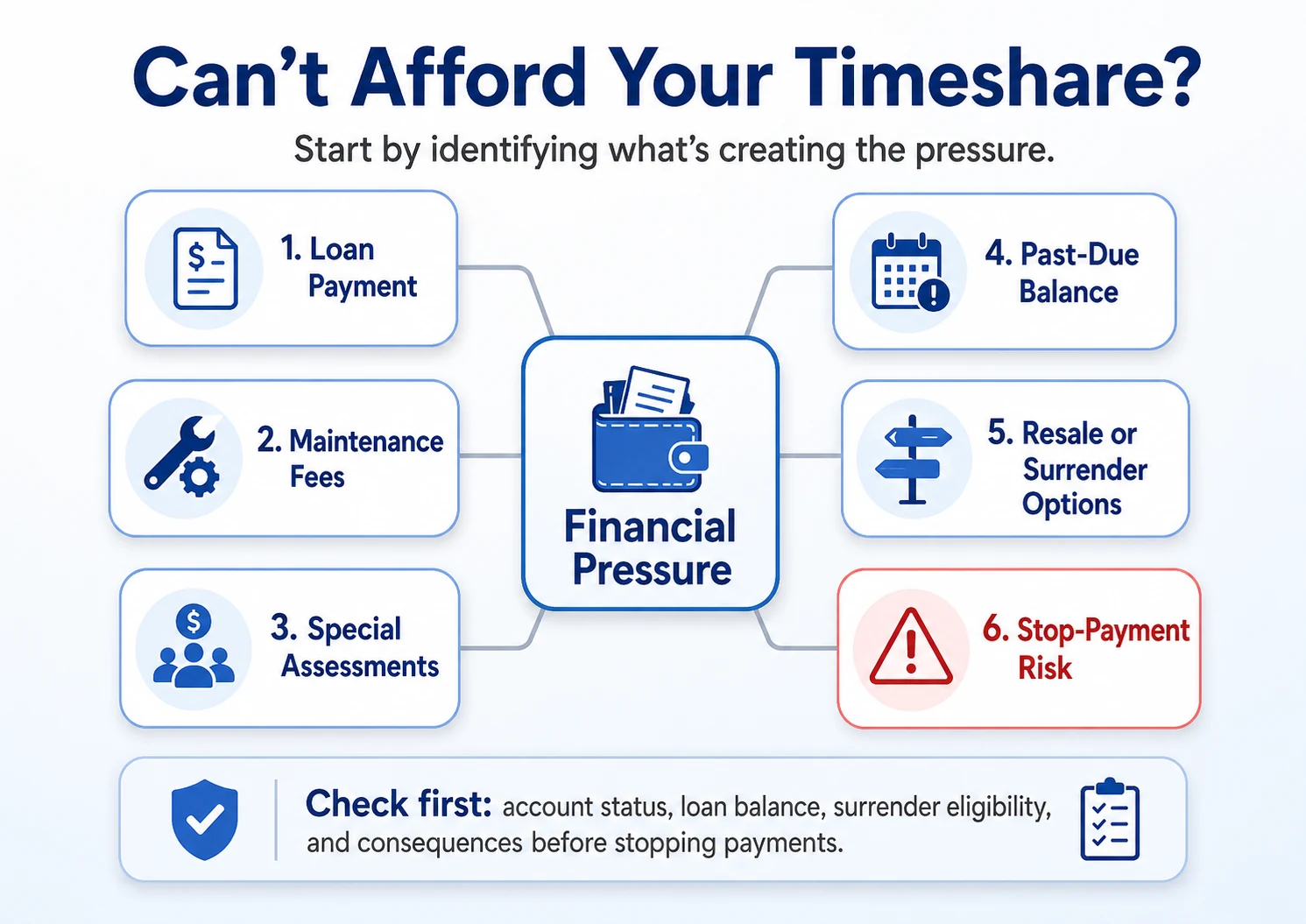

When a timeshare becomes unaffordable, the first step is not choosing an exit company or stopping payments. The first step is identifying what is creating the pressure: a loan, maintenance fees, assessments, past-due balances, reduced usage, or fear of what happens next.

Important Distinction

The Cost of Owning and the Cost of Using Are Different

Ownership costs may include the purchase loan, maintenance fees, club dues, taxes, and special assessments. Those obligations generally continue whether the owner travels or not.

Usage costs arise when the owner tries to take the vacation. Transportation, exchange fees, reservation charges, resort fees, all-inclusive costs, meals, parking, and other trip expenses can make the timeshare unaffordable even when the ownership account remains current.

Before Financial Pressure Becomes an Account Problem

Affordability Depends on the Full Cost, Account Status, and Options Still Available

A useful review should include the loan, maintenance fees, club dues, assessments, travel expenses, account standing, surrender rules, resale limitations, and the consequences of falling behind. The Timeshare Decision Intelligence Report™ helps organize those details before you stop paying, hire outside help, or make another costly ownership decision.

Need a clearer view of what is driving the financial pressure?

Review the Report Option Or continue with the affordability review belowWhat Is Making the Timeshare Unaffordable?

Not every affordability problem points to the same solution.

An owner struggling with a purchase loan may face different limitations from an owner whose loan is paid off but whose annual fees have become unmanageable. An owner who can afford the ownership bills but not the vacation itself may need to evaluate the timeshare differently from someone already receiving past-due notices.

Start by separating the financial pressure into the category that most closely reflects the current situation.

Financial Pressure Points

What Is Making the Timeshare Unaffordable?

Start by separating the pressure into categories. The right next step may be different depending on whether the issue is a loan, maintenance fees, assessments, missed payments, reduced usage, or exit uncertainty.

Payment Pressure

Loan Payments

If you still owe on the purchase loan, resale, transfer, surrender, and negotiation options may be more limited.

Annual Cost

Maintenance Fees

Rising annual fees can make ownership difficult even when the original purchase loan is already paid off.

Unexpected Cost

Special Assessments

Special assessments or one-time charges can create pressure that was not part of the original budget.

Account Status

Past-Due Balances

Once payments are late, available options may narrow and collection activity may become more likely.

Usage Problem

Reduced Usage

If you no longer use the ownership, even manageable fees may feel unreasonable compared with the value received.

High-Risk Pressure

Stop-Payment Risk

If you are considering nonpayment, review collections, credit, foreclosure, and loan consequences before acting.

A Simple Timeshare Affordability Test

A timeshare is not affordable simply because the loan payment and maintenance fee can still be paid.

The more complete test includes three categories:

1. Cost of owning the timeshare

Add the loan payment, interest, maintenance fees, club dues, taxes, assessments, and other required ownership charges.

2. Cost of using the timeshare

Add airfare or driving costs, rental cars, exchange fees, reservation charges, resort fees, all-inclusive charges, parking, meals, and other trip expenses.

3. Cost of keeping an ownership you rarely use

Consider how much is paid each year when reservations are unavailable, travel is no longer practical, or the vacation value no longer justifies the obligation.

The practical question is:

“Can I afford both the ownership and the vacations required to receive meaningful value from it?”

An owner who can pay the annual fees but cannot afford to travel may still have an affordability problem. For a fuller breakdown of these expenses, see Total Cost of Timeshare Ownership.

What to Do First If You Can’t Afford Your Timeshare

Start with the facts that determine which options may still be available.

First, confirm whether an active purchase loan remains. A financed ownership may be harder to sell, transfer, surrender, or return because many programs require the loan to be paid before ownership can change.

Next, calculate the complete annual cost. Include maintenance fees, club dues, assessments, taxes, reservation charges, and the expenses required to use the timeshare—not only the monthly loan payment.

Then verify the account status. Determine whether the account is current, recently late, in collections, or already subject to lien, foreclosure, or legal notices. Options that may be available while the account is current can become more limited after delinquency begins.

Contact the developer, resort, association, or management company directly and ask whether any written hardship, surrender, deed-back, payment, or owner-assistance program exists. Request the eligibility rules and release terms in writing.

Resale or transfer may also deserve review, but do not assume that finding a willing recipient is enough. Confirm the loan payoff, transfer restrictions, account requirements, fees, and realistic buyer demand.

The goal is to address the financial pressure before one affordability problem becomes several separate problems involving late fees, collections, credit exposure, or legal enforcement.

Keep the existing options-comparison table immediately after this section. It still serves the page well. Update its introductory line to:

The strongest option depends on whether the account is current, what remains financed, what costs are creating the pressure, and whether the proposed path actually ends the ownership obligation.

Risk Point

Stopping Payments Can Turn an Affordability Problem Into an Account-Enforcement Problem

If loan payments, maintenance fees, dues, or assessments stop, the account may move into late fees, collections, credit reporting, liens, foreclosure, termination, or other enforcement activity depending on the ownership and obligation involved.

Nonpayment does not automatically end the ownership. Before using it as a strategy, identify what is owed, what property or membership rights may be affected, and which options could disappear once the account becomes delinquent.

Before making a payment decision, slow the process down enough to understand your current position. The goal is not to pressure you into continuing payments forever. It is to help you avoid making a financial decision without knowing what may happen next.

Action Step

Build the Full Affordability Picture Before Choosing a Path

Gather the ownership, usage, and account details that determine whether the problem can be managed or whether another ownership path needs review.

- Confirm the purchase-loan balance, interest rate, monthly payment, and current payoff amount.

- Total maintenance fees, club dues, taxes, assessments, and upcoming ownership charges.

- Estimate transportation, resort, exchange, reservation, meal, and other usage costs.

- Verify whether the account is current, recently late, in collections, or subject to notices.

- Request written hardship, surrender, deed-back, payment, or owner-assistance requirements.

- Compare the cost and consequences of keeping, selling, transferring, surrendering, or stopping payments.

What If You Are Already Behind?

Once payments have been missed, affordability is no longer the only issue. The account status may begin determining which options remain available.

Still current but close to missing payments

This is usually the best time to review hardship, surrender, payment, resale, or transfer options. Some programs require the loan and annual fees to remain current.

Recently late

Request a written account statement showing the unpaid amount, late fees, due dates, and current status. Ask whether bringing the account current would preserve eligibility for any owner-assistance or surrender program.

In collections

Confirm who owns or controls the debt, what amount is being claimed, whether the developer or association still has authority to resolve the account, and whether any deadline applies. The published collection guides explain this stage in more detail.

Facing a lien, foreclosure, or legal notice

Do not treat the notice as an ordinary billing reminder. Identify the property or ownership interest affected, the response deadline, and whether the matter involves a court or formal enforcement process.

Being behind does not necessarily eliminate every option, but it can change the order of decisions. The further the account progresses, the more important it becomes to verify balances, deadlines, and proposed resolutions in writing.

Decision Insight

Financial Pressure Changes the Strategy

When money is tight, timeshare decisions can become reactive. Owners may stop paying, hire the first company that promises help, or assume the developer will not work with them. But financial pressure does not remove the need to review the structure first.

The better strategy is to identify what is driving the pressure, confirm the account status, and then compare the available options in the right order. A financed owner, a paid-off owner, and an owner already in collections may need very different next steps.

❓ Frequently Asked Questions

These questions address affordability involving the loan, annual ownership costs, travel expenses, account status, and the risks of stopping payments.

What should I do if I can’t afford my timeshare anymore?

Start by separating the purchase loan, annual ownership charges, travel expenses, and any past-due balance. Then confirm the account status and ask the developer or association whether written hardship, payment, surrender, deed-back, resale, or transfer options remain available.

Can a timeshare be unaffordable even if I can still make the payments?

Yes. An owner may be able to pay the loan and maintenance fees but no longer afford airfare, transportation, exchange charges, resort fees, all-inclusive costs, meals, or other expenses required to use the ownership.

Can I get out of a timeshare if I have very little money?

Options may be limited when a loan or past-due balance remains, but the owner should still ask the developer directly about hardship, surrender, deed-back, payment, or owner-assistance programs. Be cautious about adding a large third-party fee to an existing affordability problem.

Can I give back a timeshare because I can no longer afford it?

Possibly, but acceptance is not automatic. Many programs require the loan to be paid off and the account to be current. Request the eligibility requirements, fees, effective date, and written release terms before assuming the ownership has ended.

What happens if I stop paying my timeshare?

Missed loan payments, maintenance fees, dues, or assessments may lead to late fees, collections, credit reporting, liens, foreclosure, termination, or other enforcement. Stopping payments does not automatically cancel the ownership.

Can I sell my timeshare if I still owe money?

An active loan often makes resale or transfer more difficult because the payoff may be required before ownership can change. Confirm the payoff amount, transfer rules, buyer demand, and whether likely proceeds would cover the debt.

Should I hire a timeshare exit company if affordability is the problem?

Review direct developer options first. Before paying a third party, examine the fee, contract, timeline, refund terms, promised method, and who will perform the work. A large upfront fee can deepen the original financial pressure.

What should I do if the account is already behind?

Request a written statement showing the balance, late fees, account status, collector information, and deadlines. If the account involves a lien, foreclosure, lawsuit, or other legal notice, review that document separately from an ordinary billing or collection demand.

Bottom Line

A timeshare can become unaffordable because of more than the mortgage.

The pressure may come from financing, rising maintenance fees, club dues, assessments, travel expenses, reduced usage, or a combination of costs that no longer produces enough value.

Before stopping payments, determine what is owed, what the next vacation would realistically cost, whether the account remains current, and which written hardship, surrender, resale, transfer, or payment options still exist.

The earlier those facts are reviewed, the better the chance of addressing the affordability problem before it becomes a collections, credit, lien, or foreclosure problem.

Understand the Full Cost, Account Status, and Options That May Still Be Available

Affordability may depend on the purchase loan, annual fees, assessments, travel expenses, usage value, account standing, surrender eligibility, resale limits, and the consequences of falling behind. The Timeshare Decision Intelligence Report™ helps organize those details, identify material risks and verification gaps, and clarify which decision paths may still be realistic before you stop paying or make another costly move.

Get the Timeshare Decision Intelligence Report™ Customized ownership review • Decision-support report • No exit-company sales pitchIndependent educational decision support. This is not financial or legal advice, debt negotiation, contract cancellation, a resale service, an exit service, or a guarantee that a particular ownership option will be available.

Related Guides

These published guides can help you review the full cost of ownership, understand what may happen if payments stop, and compare options before the account escalates.

Affordability and Ownership Costs

- Timeshare Special Assessments: What They Are and When They Happen

Understand how unexpected charges can increase financial pressure beyond regular maintenance fees. - How Much Does It Cost to Get Out of a Timeshare?

Compare the potential costs associated with resale, surrender, transfer, professional review, and other exit paths.

Before and After Payments Stop

- Should You Stop Paying Your Timeshare? What Happens Next

Evaluate the difference between loan payments, maintenance fees, and other obligations before using nonpayment as a strategy. - What Happens If You Stop Paying Timeshare Maintenance Fees?

Follow how unpaid fees may progress through late charges, suspended usage, collections, liens, or foreclosure. - Can a Timeshare Go to Collections?

Understand when unpaid timeshare obligations may move from internal billing into collection activity. - What to Do After Receiving a Timeshare Collection Notice

Review the creditor, balance, deadlines, account status, and response options after receiving a collection letter.

Ownership and Exit Options

- Can You Sell a Timeshare Back to the Developer?

Learn when a surrender, deed-back, or developer take-back program may be available and what eligibility requirements may apply. - Can You Sell a Timeshare If You Still Owe Money?

Understand how an active loan and payoff requirement can limit resale or transfer options. - Timeshare Exit Guide: How to Get Out of a Timeshare

Compare resale, surrender, deed-back, transfer, developer programs, and other possible exit pathways.