Timeshare Review and Research Guide

Timeshare Reviews: How to Evaluate Companies, Complaints, and Owner Experiences

Timeshare reviews often appear contradictory because owners and guests may be describing entirely different parts of the experience.

One review may praise the resort, staff, and vacation. Another may describe sales pressure, rising fees, booking frustration, resale difficulty, or an unresolved exit concern. Both experiences may be genuine without answering the same question. This guide helps you identify what a review is actually describing, recognize recurring patterns, and find the company-specific research most relevant to your decision.

About this guidance: Timeshare Travel Club Authority’s guidance draws on experience with vacation-club structures, resort operations, sales practices, financing, maintenance fees, booking systems, customer service, resale limitations, ownership transfers, surrender programs, and exit-related concerns. Owner experiences can vary by resort, company program, legacy system, contract, purchase date, ownership type, account standing, and individual circumstances, so reviews should be used to identify patterns and questions that can then be checked against the relevant documents and current account information.

Review Research Paths

Choose What You Want to Research

Timeshare reviews can answer different questions depending on whether you are researching one company, trying to interpret complaints, or comparing two vacation ownership programs. Start with the path that best matches what you need to understand.

Find a Specific Timeshare Company Review

Browse detailed guides for major vacation clubs, developers, points systems, legacy programs, and membership-based resort companies.

Browse company review guides → 02 Review InterpretationUnderstand Complaints, Ratings, and Owner Experiences

Learn how to separate resort reviews from concerns involving sales practices, fees, booking, resale, transfers, customer service, or exit difficulty.

See how to read reviews → 03 Side-by-Side ResearchCompare Timeshare Companies

Compare major programs by ownership model, booking access, annual costs, resale rules, transfer restrictions, and long-term flexibility.

Compare timeshare companies →Company Review Guides

Find the Review Guide for Your Timeshare Company

Use these company-specific guides when you want to research one vacation club, developer, points system, legacy program, or membership-based resort company. Each guide focuses on the ownership structure, annual costs, booking concerns, resale limitations, transfer rules, and possible exit considerations connected to that program.

Major Vacation Club Systems

Start here if you own or are considering a large points-based vacation club, deeded timeshare program, or branded resort ownership system.

Marriott Vacation Club

Review ownership structure, maintenance fees, resale considerations, and exit-related contract issues.

View guide → Vacation ClubHilton Grand Vacations

Review club structure, related programs, resale issues, transfer limits, and exit considerations.

View guide → Points SystemClub Wyndham

Review Wyndham points, booking rules, maintenance fees, resale realities, and ownership risk factors.

View guide → Credits SystemWorldMark by Wyndham

Review WorldMark credits, dues, booking access, resale considerations, and exit-related issues.

View guide → Regional ClubClub Wyndham South Pacific

Review South Pacific ownership, annual fees, resale limits, transfer issues, and exit considerations.

View guide → Vacation ClubDisney Vacation Club

Review DVC points, annual dues, home resort priority, resale rules, ROFR, and exit considerations.

View guide → Vacation ClubHyatt Vacation Club

Review Hyatt, former Hyatt Residence Club, former Welk, fees, resale limits, and exit options.

View guide → Vacation ClubWestin Vacation Club

Review Westin ownership, Marriott Vacation Clubs connections, annual fees, resale limits, and transfer rules.

View guide → Vacation ClubSheraton Vacation Club

Review Sheraton ownership, Vistana history, annual fees, resale issues, and transfer considerations.

View guide →Resort and Developer Review Guides

Use these guides if your issue is tied to a specific developer, legacy resort company, points program, or resort ownership system.

Westgate Resorts

Review ownership structure, financing exposure, transfer limits, resale concerns, and surrender considerations.

View guide → Points SystemBluegreen Vacations

Review Bluegreen points, annual fees, resale limitations, transfer rules, and exit-related considerations.

View guide → Legacy SystemDiamond Resorts

Review Diamond legacy ownership issues, fee obligations, resale limits, and Hilton-related considerations.

View guide → Vacation ClubHoliday Inn Club Vacations

Review fees, points, booking rules, resale limitations, and exit options for Holiday Inn Club Vacations owners.

View guide → Resort SystemExploria Resorts

Review Exploria ownership, fees, resale challenges, transfer issues, and exit-related considerations.

View guide → Vacation ClubCapital Vacations

Review Capital Vacations ownership, club fees, resale realities, transfer limits, and exit considerations.

View guide →Mexico and Membership Club Programs

These guides focus on membership-style vacation programs, right-to-use structures, and resort clubs that may operate differently from traditional deeded timeshares.

Palace Elite

Review Palace Elite membership structure, fees, usage limitations, resale concerns, and exit considerations.

View guide → Membership ClubVida Vacations

Review Vida Vacations membership terms, usage rights, fees, transfer limits, and exit-related issues.

View guide → Vacation ClubRoyal Holiday Vacation Club

Review membership structure, annual fees, points, booking limits, resale issues, and exit considerations.

View guide →These guides are not general star ratings. They focus on the ownership issues that usually matter most after the sale: fees, financing, resale limits, transfer rules, booking restrictions, and realistic exit options.

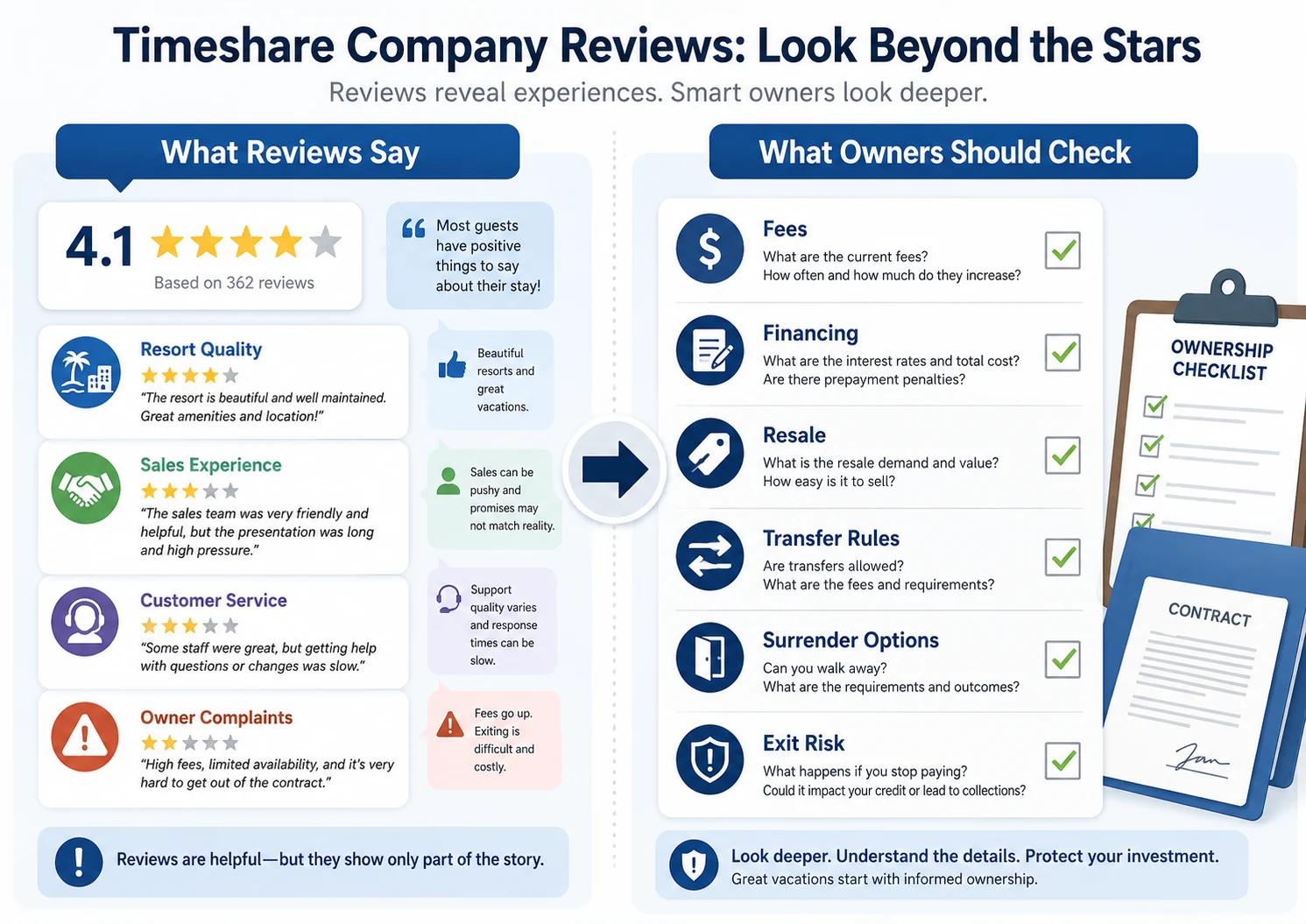

Why Timeshare Company Reviews Are Often So Mixed

Timeshare company reviews often appear contradictory because owners are not always reviewing the same part of the experience.

One person may be describing a resort stay. Another may be describing the sales presentation. Someone else may be reviewing years of maintenance fees, booking frustration, customer service problems, resale attempts, or difficulty obtaining a clear answer about surrender or exit options.

Those experiences can all be genuine.

A family that enjoyed a clean resort, helpful staff, and a convenient location may leave a positive review. That review can help evaluate the vacation experience, but it does not explain whether the ownership remains affordable over time, whether the promised availability is realistic, or whether the interest can later be transferred.

A frustrated owner may leave a negative review after encountering rising costs, reservation problems, resale limitations, or exit difficulty. That complaint may identify an important pattern, but the outcome may also depend on the owner’s contract, purchase date, financing, account status, and specific program.

That is why reviews should be interpreted by the issue being described, not simply by the number of stars.

Important Distinction

Resort Reviews and Ownership Reviews Are Not the Same Thing

A timeshare company may operate attractive resorts with helpful staff, desirable locations, and satisfied vacation guests while still offering ownership contracts that require careful review. Resort quality describes the travel experience. It does not automatically explain the financing, annual costs, booking rules, resale limitations, transfer requirements, or possible exit options attached to the ownership.

The reverse is also true. A negative complaint may describe a serious problem, but it may not apply to every owner, resort, contract, or legacy program connected to the company. The useful question is what the review is actually about—and whether that issue appears in the ownership you are researching.

Review Interpretation

What Type of Timeshare Review Are You Reading?

A five-star resort review and a one-star exit complaint may both be accurate, but they describe different parts of the ownership experience. Identify the issue behind the review before deciding what it means.

Resort Experience Reviews

These reviews usually focus on room quality, amenities, location, staff, cleanliness, restaurants, pools, and general vacation enjoyment.

Sales Presentation Complaints

These reviews may describe pressure, long presentations, upgrade pitches, unclear explanations, or differences between what was discussed and what the owner later understood.

Fee and Billing Complaints

These reviews may involve maintenance-fee increases, club dues, assessments, reservation charges, late fees, billing disputes, or collection notices.

Booking and Availability Reviews

These reviews often describe difficulty reserving the expected dates, destinations, unit sizes, or resorts within a points or vacation club system.

Resale and Transfer Complaints

These reviews may come from owners who tried to sell, give away, transfer, or deed back an ownership and discovered restrictions or limited buyer demand.

Exit Difficulty Reviews

These reviews may involve surrender requests, deed-back eligibility, exit companies, payment decisions, loan balances, or uncertainty about whether the ownership has ended.

Once reviews are separated by type, the apparent contradictions become easier to understand. A company may receive strong resort feedback while also generating complaints about fees, booking, resale, or exit options. The goal is not to average those experiences into one score. It is to identify which patterns may matter to the ownership decision.

System Insight

Complaint Patterns Are Signals—Not Contract Conclusions

- Repeated complaints can identify an issue worth investigating, such as fee increases, reservation difficulty, sales confusion, transfer limits, or exit frustration.

- The same company may operate several clubs, resorts, trusts, and legacy programs with different rules and owner experiences.

- A complaint may be accurate without applying to every contract, purchase date, ownership type, or account.

- A positive rating may describe the resort rather than the ownership, financing, annual cost, resale market, or long-term flexibility.

- The review should guide the question to verify; the ownership documents and current account determine the answer.

How to Use Timeshare Reviews Before Buying or If You Already Own

The value of a review depends partly on where you are in the ownership decision.

Before Buying

Reviews should help you identify what needs to be verified before signing—not simply reassure you that the resort is popular.

Look for recurring comments about:

- How the ownership was explained during the sales presentation;

- Whether booking access matched the buyer’s expectations;

- How maintenance fees, dues, and other charges changed over time;

- Whether benefits were documented or described only verbally;

- How resale buyers are treated;

- What transfer approval or fees may apply; and

- Whether the company offers a written surrender or deed-back process.

Then compare those concerns with the actual documents being offered.

Confirm what you would own, what it may cost after the first year, how reservations work, what happens to benefits on resale, and what options may exist if the program later stops fitting your travel or finances.

If You Already Own

Reviews can help current owners recognize pressure points, but they should not create panic or lead you to assume another owner’s outcome will be yours.

Compare the complaint with your own facts:

- If reviews mention rising fees, examine your billing history.

- If owners describe booking difficulty, review your points level, booking window, home-resort rights, and travel flexibility.

- If complaints involve resale, check your transfer rules and whether resale buyers lose benefits.

- If owners describe exit problems, confirm your loan balance, fee status, account standing, and written surrender eligibility.

- If complaints mention collections or credit concerns, determine whether your own account is current, delinquent, or already with an outside collector.

The useful question is not simply whether other owners are unhappy. It is:

Do the issues described in those reviews match the structure and status of my ownership?

Risk Point

Reviews Can Reveal a Problem Without Confirming Your Options

Timeshare reviews may identify recurring concerns involving fees, booking, customer service, sales expectations, resale difficulty, or exit limitations. But they cannot confirm what your contract requires, whether your account qualifies for a particular option, or whether another owner’s outcome applies to you.

The risk is acting on a review before checking the ownership behind it. An owner may assume surrender is available, stop paying because others did, hire an exit company, or abandon a realistic transfer option without first confirming the loan balance, fee status, program rules, and written resolution requirements.

Reviews work best as an early-warning system. When the same concern appears repeatedly, investigate it—but compare the pattern with the documents and account information that control your own situation.

Action Step

Match the Review to the Terms That Control the Ownership

Before relying on a positive rating or negative complaint, identify the issue being described and verify whether that issue appears in the contract, billing history, booking rules, or account you are reviewing.

Identify whether the review concerns the resort, sales process, fees, booking, customer service, resale, transfer, or exit difficulty.

Compare fee complaints with the maintenance fees, dues, taxes, assessments, and other recurring charges attached to the ownership.

Check whether booking complaints involve home-resort priority, reservation windows, points requirements, inventory, or limited travel-date flexibility.

Review resale and transfer complaints against the contract’s approval rules, fees, buyer restrictions, and benefit limitations.

Verify whether exit complaints involve an unpaid loan, delinquent fees, ineligible ownership type, or lack of a written surrender program.

Look for patterns across multiple detailed sources rather than relying on one highly positive or highly negative review.

Even after reviews have been categorized and compared with the available facts, the most important question is whether the ownership itself shows signs of financial, usage, transfer, or exit pressure.

Free Ownership Review Preview

Do the Concerns in the Reviews Match Your Ownership?

Reviews may point toward common problems, but the practical importance of those concerns depends on your financing, ownership type, annual costs, booking rights, resale restrictions, account standing, and possible surrender options.

Identify which ownership factors may create the greatest pressure.

Review possible limits affecting usage, transfer, resale, or surrender.

See which contract and account details may deserve closer investigation.

Move from general company reviews to a clearer preview of your own ownership factors.

Try the Free Ownership Risk Profile™Free preview • Educational decision support • No exit-company sales pitch

A Risk Score can help identify pressure points, but reviews still require interpretation. The next step is understanding when company reputation is useful context — and when it can distract from the actual ownership terms that determine your options.

❓Frequently Asked Questions

Timeshare company reviews can be useful, but they often mix resort experiences, sales complaints, fee frustration, booking problems, resale limitations, and exit concerns. These answers explain how to read reviews without assuming every comment applies to the same company program or ownership.

Are timeshare company reviews reliable?

Timeshare reviews can provide useful context, particularly when they clearly explain what happened, when it happened, and which part of the experience caused the praise or complaint.

A review is less useful when it gives only a star rating or general opinion without identifying whether the issue involved the resort, sales presentation, fees, booking, resale, transfer, or exit process.

Why do timeshare companies have so many mixed reviews?

Reviews are often mixed because owners and guests are reviewing different experiences. One person may be rating the resort, while another is describing financing, maintenance fees, booking difficulty, customer service, resale problems, or an unsuccessful surrender request.

Those experiences can all be accurate without producing one simple conclusion about every ownership connected to the company.

Should I trust complaints about a timeshare company?

Complaints should be treated as signals rather than automatic conclusions. If multiple owners describe the same issue, such as fee increases, reservation problems, sales confusion, transfer limits, or exit difficulty, that issue deserves closer investigation.

The next step is confirming whether the same concern appears in the program, contract, account, or purchase you are evaluating.

Does a highly rated timeshare company mean the ownership is low-risk?

Not necessarily. A company may operate desirable resorts and receive strong hospitality reviews while still offering ownerships with financing, rising annual costs, booking competition, resale restrictions, or limited exit options.

Resort satisfaction and ownership flexibility should be evaluated separately.

What should I look for in timeshare reviews before buying?

Look for detailed comments about sales expectations, annual fees, points value, booking access, resale treatment, transfer rules, customer service, and whether important benefits were documented.

Use those comments to create questions for the sales representative and compare every answer with the written ownership documents before signing.

How should current owners use timeshare reviews?

Current owners should compare the issue in the review with their own contract, billing history, reservation experience, financing, account standing, and transfer rules.

A complaint can identify something to investigate, but it should not cause an owner to assume that another person’s solution, default experience, or exit outcome will apply to the account they hold.

Can reviews tell me whether I can get out of my timeshare?

No. Reviews may reveal recurring concerns about resale, transfer, surrender, or exit difficulty, but they cannot confirm which options are available for a specific ownership.

Exit options may depend on the ownership type, loan balance, maintenance-fee status, account standing, transfer restrictions, and whether the company offers a written surrender or deed-back process for that program.

Are timeshare reviews the same as comparing timeshare companies?

No. Reviews provide context about owner experiences, complaints, resort satisfaction, service, and recurring concerns. A company comparison evaluates two or more programs using consistent factors such as ownership structure, booking, annual costs, resale rules, transfers, and exit considerations.

Use the Timeshare Companies Compared guide when your main goal is evaluating how programs differ.

Bottom Line

Timeshare company reviews can be helpful, but they are rarely reviewing one single thing.

Some reviews describe resort quality and vacation satisfaction. Others reveal concerns involving sales expectations, customer service, annual fees, booking access, resale difficulty, transfer rules, or exit options.

A positive resort review may be accurate without explaining the long-term ownership obligation. A negative complaint may identify a serious issue without applying to every contract or program operated by the company.

The most useful approach is to read reviews by category, look for detailed patterns, and then verify the issue against the ownership being considered or held.

Before acting on a review, confirm:

- What part of the experience the reviewer is describing;

- Whether the same issue appears across multiple credible sources;

- Which company program, resort, trust, or legacy system is involved;

- Whether the concern appears in the contract, billing history, or booking rules;

- Whether financing or account standing changes the available options; and

- What written documentation would confirm the resolution being considered.

Company reputation is useful context. The ownership documents and current account determine what the review may mean for your decision.

Look Beyond the Reviews

Understand What Your Own Timeshare Documents and Account Actually Show

Company reviews can reveal recurring concerns, but your decision depends on the ownership you hold or are considering. The Timeshare Decision Intelligence Report™ helps organize your documents, ownership structure, financing, annual costs, booking rights, resale restrictions, transfer rules, verification gaps, and possible decision pathways before you act on general reviews or another owner’s experience.

Get the Timeshare Decision Intelligence Report™ Customized ownership review • Document and account analysis • No exit-company sales pitchIndependent educational decision support. This is not legal advice, contract cancellation, an exit service, a resale service, lender negotiation, debt settlement, or a promise that a timeshare can be exited.

Related Guides

Reviews can help identify recurring concerns. These guides explain several of the ownership issues those reviews frequently raise:

Ownership Costs and Usage

- Timeshare Maintenance Fees: Why They Keep Increasing

Understand why annual costs rise and how fee pressure may affect long-term ownership. - Why Is It So Hard to Book a Timeshare?

Review how points, booking windows, inventory, and owner priority can affect availability.

Resale and Exit Concerns

- Why Are Timeshares So Hard to Sell?

Learn how supply, buyer demand, fees, and transfer restrictions affect the resale market. - Timeshare Exit Options Compared

Compare surrender, deed-back, resale, transfer, and other potential exit paths. - How to Get Out of a Timeshare Legally

Understand what documentation shows that an ownership has actually been transferred, surrendered, canceled, or otherwise resolved.